Build Alpha: Basic video explaining and testing Moving Average Convergence Divergence (MACD) on some popular Exchange Traded Funds (ETFs) such as: SPY, QQQ, TLT, GLD and more.

Wednesday, 2 September 2020

Tuesday, 2 June 2020

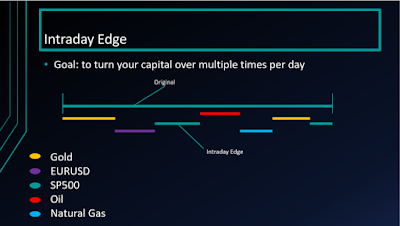

Intraday Edge: Find strategies backwards

A large

consideration of developing trading systems should be how efficient our

capital is working for us. The quicker we can realize profits, the more

trades we can make thus allowing our capital to compound more quickly.

Additionally, sitting in positions for long periods increases our risk

to extraneous events.

More

importantly, it is typically easier to find daily or higher timeframe

edges than intraday edges due to the increased noise in intraday data.

Is there a way

to reduce the time in a position which would increase our trade count

(via number of strategies) which would then allow us to arrive at the

law of large numbers more quickly and therefore allow our capital to

compound more quickly?

Yep. One of the new features in Build Alpha,

called “Intraday Edge”, is a tool which allows us to do exactly that.

It allows us to dig deeper into daily trading strategies to see if we

can make them more efficient by reducing their holding times into

smaller intraday time windows. Maybe we can capture most of the daily strategy’s edge during only a small portion of the typical holding time. That’s right.. turning daily strategies into intraday strategies.

A simple example can help clarify the power of this new feature…

First, let’s

take an original daily trading system. I will use a simple one rule

strategy that goes long the SP500 futures contract whenever the trading

session closes in the bottom 20% of the day’s range (internal bar

strength or internal bar rank – IBR in Build Alpha). We then hold that

long position for 1 day. This assumes about a 23 hour risk (i.e., one

Globex trading session).

However, what

if we could dig into this strategy and realize that most of the gains

only come from 1 am EST to 4 am EST? We can then reduce our holding time

by about 87% which now only ties up our capital for 3 hours as opposed

to 23! This gives us an additional 20 hours to utilize other strategies

to continue to grow our capital while still capturing a large portion of

the original daily strategy’s edge.

Imagine we

only had enough capital for one strategy. This Intraday Edge feature can

now make our capital work much harder by finding intraday edge

strategies for multiple markets/times of the day. Tying up capital for

23 hours in one daily strategy vs. trading 7 different intraday edge

strategies with the same capital.

*Original strategy can be

reduced by Intraday Edge which allows other intraday strategies to be

traded with the same capital that was orignially tied up by the daily

strategy*

In the end, it makes our once daily

system much more efficient. Check out the performance metrics of the

original daily system compared to the new “Intraday Edge” version.

- Highlight any daily strategy

- Click the Test Settings in the bottom right to configure the intraday timeframe you want to use

- Hit the Intraday Edge button

BuildAlpha

will then search all possible holding periods within the original

strategy’s trading duration to see if there is a more efficient version

with reduced holding times. You can include the original strategy’s exit

criteria such as stops, etc. or choose to exclude them. Flexibility to

test everything is always key in Build Alpha.

Intraday Edge can even be used on

different markets at the same time. For example, imagine an original

system built on Gold daily bars but then we search for an intraday edge

version that trades oil but only during this specific 2 hour window

while the original Gold System has an active signal.

This Intraday Edge feature essentially

allows us to search for intraday and multi-timeframe strategies in a new

way. In this above Gold and Oil example we have a multi-timeframe AND

intermarket strategy created from a simple Gold daily strategy.

You can still search for multi-timeframe

and intraday strategies in the original/traditional way. That is, just

searching the intraday data from the start. However, it is often faster

and easier to find daily strategies then work them into intraday ones.

At least now with Build Alpha you have the option to search both ways. Something not possible elsewhere.

And of course, all of the adjustments

from the Intraday Edge feature are then applied to the code generators

so you can automate these Intraday Edge systems with one click as with

everything.

As always, I will keep attempting to add

flexibility and ways to dig deeper so we can have the best trading

strategies possible. Leave no stone unturned and test everything!

Thanks for reading,

David

Noise Test Parameter Optimization

In short, this

is a new feature that allows us to optimize strategies across noise

adjusted data series as opposed to the traditional method of

optimization which only optimizes across the single historical price

series.

The problem we face is the historical data is merely only one possible path of what *could* have happened. We need to prepare ourselves for the probable future not the certain past. In

order to do this, we can generate synthetic price series that have

altered amounts of noise/volatility than the actual historical data.

This provides us with a rough sample of some alternate realities and

potentially what can happen going forward. This is the exact type of

data that can help us build more robust strategies that can succeed

across whatever the market throws at us – which is our end goal in all

of this, right?

Let’s look at a Noise Test Parameter Optimization (NTO) case study to show exactly how it works…

I have built a strategy from 2004 to 2016 that does quite well. The strategy’s performance over this period is shown below…

Now, if we

right click on the strategy and select optimize, we can generate a

sensitivity graph that shows how our strategy performs as we alter some

parameters. This is done on the original historical price data with no

noise adjusted data sample added (yet). We simply retrade different

variations of parameter settings on the single historical price data and

plot the respective performances. This is how most platforms allow you

to optimize parameters and I want to show how misleading it can be to

traders. The rule I’ve optimized had original parameter values of X = 9

and Y = 4 (black arrow). The sensitivity graph is shown below. Each plot

consists of three points: parameter 1, parameter 2 and the resulting

profit.

Build Alpha:

We can see the original parameters are near a sensitive area on the

surface where performance degrades in the surrounding areas. Performance

drops pretty hard near our original strategy’s parameters which means

slight alterations to the future price data’s characteristics can

degrade our strategy’s performance quite a bit. Not what we want at all

and, as we all know, there will be alterations to future price’s

characteristics! How many times has a backtest not matched live results?

Perhaps more robust parameter selection can help

The more

robust selection using the typical simple optimization method on the

historical data shows we should probably pick a parameter more near X = 8

and Y = 8 (pictured arrow below). This is the traditional method taught

in textbooks, trading blogs, etc. We optimize on the single historical

data then find a flat/non-peaked area close to our original parameters

and use those new parameters.

However, if we run BuildAlpha’s

Noise Test Optimization with up to 50% noise alterations and 50 data

samples (green box below), we see a much different picture. What this

does is, instead of optimizing on one historical path we now optimize

across the one historical path AND 50 noise altered data series. The

sensitivity graph shows a much different picture when optimized across

the 51 data series. We are less concerned with the total profit and loss

but rather the shape of the surface…

Originally Posted: http://buildalpha.com/noise-test-parameter-optimization

Originally Posted: http://buildalpha.com/noise-test-parameter-optimization

Friday, 15 May 2020

Make Task Investing Easy

Investment in

stocks in such a volatile market nowadays has become a cause of concern

and how to manage one’s finances. Most of the people ask their fund

managers to invest in quality stocks at this point in time. Which is the

best asset class to invest in and how to manage your portfolio? Some

people think that investment is the most straightforward aspect of

financial planning, whereas nobody knows the correct answer and is

debatable. But now, with the advancement of technology, things have

become quite more comfortable and if we look at the broader pictures

with investing tools like Build Alpha, it is far easier to invest and trade with the best expertise available with you at every point of time.

Investment in

the capital markets can be comparatively easier than other asset classes

or yield drivers. One should invest smartly and systematically keeping

in view the returns on your investment, but most of the investors do it

otherwise, and everything is turned around like not placing the

upside-down cake correctly, thus the toppings at the bottom scatters.

With a tool like Build Alpha now investing activity has become way

easier as it gives proper analysis of the trend of the market.

Especially for

the new age investors who have just entered the market, they can

quickly get the knowledge in the simplified version through this unique

tool. It is very user friendly and an easy to access tool that serves

just perfect for solving the queries and dilemmas of new as well the

experienced traders and investors. Even if you are dealing in the market

for long-term, there ought to be something or the other that may bother

you or you may not understand as the market is quite volatile and it is

quite difficult to depict the pattern well.

Here is where BuildAlpha

comes into play by helping you out with that uncertain motions of the

market where you fear to take your next steps. As with unpredicted

levels and economic uncertainty of course comes a lot of risks. Build

Alpha can help you identify these risks to hopefully sidestep them

before they affect your portfolio.

Very well

written by Warren Buffet, there are lots of ups and downs in the stock

market, and one should be patient. That is why he termed the capital

market where investing is a no-called-strike game. So now, with this

unique and very useful tool, it has become much simpler to invest in the

capital markets and earn money, and the same time the fear of losing

will be minimized as now you have experienced moves, tested them and are

ready for the next one. Therefore, do the research of the markets with

the help of Build Alpha before you are interested in investing and before new risks hit the market.

Originally Posted: http://buildalpha.us/make-task-investing-easy/

Friday, 8 May 2020

Volatility Filters Into Stock Market Decline

The recent volatility, like all volatility events, has brought some traders a fortune and others pain.

The ability to identify volatility regimes is paramount!

Correct

identification of volatility shifts gives one the ability to adjust

size, turn strategies off, enable hedging strategies, etc.

Ideally, a

trader should have strategies for every market regime. If one can

identify which regime and price action characteristics are likely (or

unlikely) then plenty of stress can be removed and a certain level of

robustness is added to the trader’s portfolio.

In this post, I

want to discuss four ‘volatility identifiers’ that can hopefully be

used to either avoid or capitalize on the next volatility event.

These have been powerful indicators to add to trading systems to help decide when on/off, filtering and of course sizing.

Are they a be all end all? No.

Are they predictive? No.

Are they a holy grail? No.

Should you ignore them? No!

I will only

examine these volatility regimes based upon tomorrow’s range and

tomorrow’s return.

They can of course be expanded to look at 5 days

forward, 20 days forward, etc. but this is left up to the reader.

Plotted below

is how these volatility identifiers affect the S&P 500’s next day

range and return. The X-axis is the volatility identifier and the Y Axis

is the S&P 500 range (or return) for the next day.

BuildAlpha:

In short, the level of these volatility identifiers has a BIG impact on

what you can expect for tomorrow’s session and thus your trading

systems can/should take a look to see if these can help improve

performance or even alert to when some strategies should be ‘offline’!

1)

Treasury Spreads vs. S&P 500 Futures. When the 10-year yield minus

the 2-year yield is too flat or too steep things tend to get

volatile. The x-axis is the basis points of this spread. This is the

only goldilocks identifier in this post where volatility increases at

both extremes of this indicator but mellows out in the middle of the

range.

2)

Whenever the front month VIX futures contract is trading above the

second nearest month by more than 5-10% things tend to get volatile.

Here is the VIX futures curve in March of 2019 vs. March 2020 as well as

the contango percent.

3)

Whenever SPX index’s option gamma exposure (GEX) is negative things

tend to be more volatile. Gamma exposure is the total sum of gamma

(option greek) multiplied by open interest of the calls minus the sum of

gamma multiplied by the open interest of the puts. This gives us a

sense of where/how option market makers are positioned. When GEX is

negative things tend to get volatile.

4)

Whenever the S&P 500 components’ gamma exposure is negative things

tend to be more volatile as well. Obviously very correlated to #3 but

important to note the distinction. This is like above but is the

aggregate of the actual options on the ~500 stocks in the index vs. the

options on the index itself.

There are

other volatility identifiers such as Dark Pool Index (DIX), counting the

number of S&P 500 stocks above/below the 50 day moving average,

number of new highs vs. new lows, economic data filters, etc.

Also, to be fair, Gamma Exposure and Dark Pool Index were first published here: https://squeezemetrics.com/download/white_paper.pdf and pointed out to me by a bunch of Build Alpha users. I want to give credit to where it is due.

In the latest Build Alpha update

all of these volatility identifiers, economic data and market breadth

filters will be included and testable at the click of a button. Even

possible to automate them as part of your strategies built and/or

improved by Build Alpha.

I am looking forward to a post COVID world

and what the market will bring us on the other side. Be prepared! Any

questions please contact me at david@buildalpha.com

Tuesday, 5 May 2020

Build Alpha Update

Build Alpha: In the latest update it is now easier than ever to modify the built-in signals, optimize parameters across noise adjusted data series and other symbols, create rebalance strategies, search for intraday edges and new signals including Gamma Exposure, Dark Pool Index and more.

Tuesday, 7 April 2020

Ideal Investing Tool

Trading and Investing is not an easy job and it is

best if you have an expert’s advice or better yet a true quantified

edge. To gather expert advice and quantified edge, there is a unique

tool on the market which is designed specifically for trading and

investing purposes. It will serve the purpose for the new investors, and

for the existing ones who are experienced in providing them with expert

advice, new methods of testing and validation. Build Alpha is the ideal software that will help you creating a trading or investing plan that experts would be proud of.

With this best investing tool, you inevitably live in

the golden age of stock market investing. You will get unlimited

information, which everyone can reach who is using the software. Build

Alpha provides unparalleled data, signals and testing methods to help

you build the best trading or investing strategies. It is such a unique

tool which will help you in many ways.

It is very economical and is of great tool which

small investors are taking great advantage of. These small investors

spend next to nothing for tools, the best investing tools, and

knowledge. If you’re someone who is invested in the stock market, you

should surely look at BuildAlpha. It can even help you analyze your existing trading or investing strategies as well as help you create new ones.

Features of Build Alpha Investing Tool

1. The first advantage that you get from this tool, Build Alpha

is the ability to test thousands of trading and investment signals

without having to write any code yourself. You can select from

candlestick patterns, technical indicators, volume, market breadth

studies, intermarket signals, multi-timeframe signals and much more to

test, create and build your perfect investment strategy – all is done

point and click with no programming. This gives the trader and investor a

significant advantage because of the amount of time saved.

2. Free Portfolio Analysis – Another

feature that you should check for is the portfolio analysis or

Portfolio Mode. With the help of Build Alpha, all the aspiring investors

can analyze their portfolios for prospect and opportunity. This

portfolio analysis tool will not cost a lot of money and will give you a

lot of investing tools and tests you can use. It will offer you

tremendous robust analysis tools. These tools possess a piece of expert

advice which actually feels like it contains various experts. The tools

also allow you to run simulations, find efficient quantitative test and

factor-based financing models.

Individual stock investors can use this software for

to find the best portfolio for their risk return desires. Investors can

track trades, calculate risk-adjusted revenues, and conduct quantitative

research. It will also assist you in maintaining your portfolio as a

whole rather than just your individual strategies and positions.

3. Education of Investors

To compete in today’s market, traders and investors

need proper tools and education. Build Alpha comes complete with private

training video course to assist new and advanced traders and investors

on how to properly build strategies, test them and construct proper

portfolios for individual risk/reward characteristics. This is an all in

one tool that comes complete with training. This gives Build Alpha users significant advantage over their counterparts still attempting to learn and build strategies manually.

Originally Posted: http://buildalpha.us/ideal-investing-tool/